5 Essential Considerations For Mortgage When Acquiring Your Dream Home

1

Eligibility

Before a bank decides to approve your home loan, you need to meet certain eligibility requirements, for example

Annual or Monthly income

Buyer’s minimum and maximum age

Loan quantum

Residency status

Fulfilment of the Monetary Authority of Singapore’s property loan rules and HDB’s/the bank’s internal credit requirements eg TDSR

2

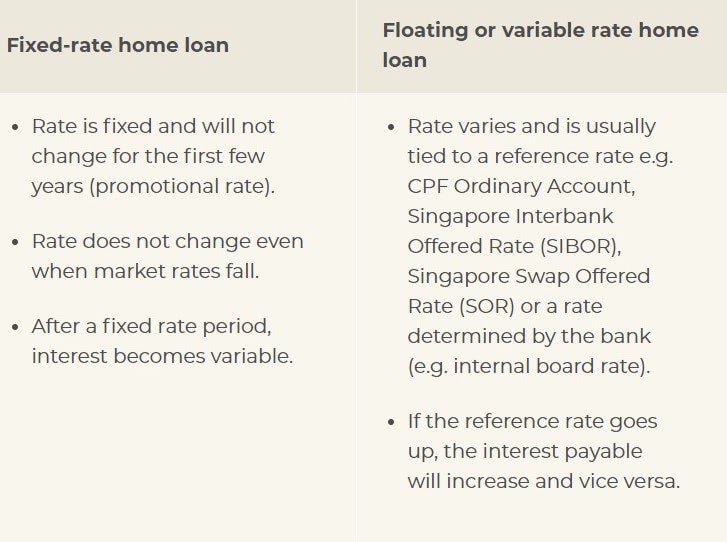

Fixed Vs Floating Rate

3

Benchmark rates

Popular benchmark rates used here includes the Singapore Interbank Offered Rate (SIBOR) and Swap Offer Rate (SOR).

In the last few years, banks have started offering various innovative benchmark that may offer some advantage to consumers. For instance, a type of home loan that is pegged to the bank’s Fixed Deposit rate. This provides a good alternative for those who thinks that interest rates will rise, as fixed deposit rates will likely rise at a slower rate compared to the SOR or SIBOR.

4

Loan Conditions

Borrowers also need to be aware of the conditions attached to their mortgage so that they will not be caught by surprise should they consider the option to refinance or sell later. These conditions can affect the cost and can negate the potential cost savings.

Pre or full payment penalty during lock in period

Claw-back for free fire insurance, valuation report, legal subsidies & etc

5

Mortgage Insurance

A mortgage insurance provides coverage for the outstanding home loan amount in the unfortunate situation where the borrower dies or become total and permanently disabled. The borrower and his family can potentially lose their home if they become unable to service the home loan. So to provide a peace of mind, especially if the borrower is shouldering the main loan burden, it could be a smart move to take up a mortgage insurance.